Initiating Coverage [ACTIONABLE IDEA #5]: Riken Keiki

An undervalued and misunderstood recurring revenue semiconductor beneficiary gas detection company trading at half the multiple of peers.

Hello Capital Light readers!

Capital Light has discovered a potential opportunity in a high-quality Japanese stock trading at an attractive valuation for its quality, recurring revenue nature, and growth prospects.

Conviction Level: Medium

Risk Level: Low-Medium

This idea has the following characteristics:

Moderate liquidity (100k shares/day, ¥385M ($2M USD)/day) making this idea suitable for small-medium funds and most individual investors.

A fortress balance sheet with about 17% of the market cap in cash and liquid securities.

A cash-adjusted P/E under 15 and an EV/EBIT of 11.

This company remains an undiscovered AI beneficiary selling to semiconductor companies and datacenters (40% of revenue), which remains diversified through other sector exposures (combined 60% of revenue) as well.

Percentage revenue growth in mid single digits to mid teens.

Capital Light believes there is earnings upside and multiple upside from ¥3500 per share today to ¥4,700 per share (+32%) based on a 16X EV/EBIT fair value multiple immediately, and as much as ¥4900 (+40%) per share in a 2027 base case. A bull case puts shares as high as ¥6900 (+97%) in a 2027 bull case.

Let’s dive in!

Introduction

Riken Keiki (Tokyo Stock Exchange: 7734) is a Japanese company that manufactures and sells critical industrial gas detection and alarm equipment. At first glance, Riken Keiki initially appears to be a basic commoditized hardware manufacturer. In reality, Riken Keiki is a specialized hardware sales business with attached replacement, maintenance, and service revenue, resulting in a high-quality recurring revenue model. Riken Keiki is effectively a razor-and-blades business model company valued like an industrial commodity company.

Capital Light believes there is immediate 33% upside to a fair value of ¥4,750 per share and up to 100% upside to ¥6900 per share if a medium-term bull case materializes.

Business History

Riken Keiki’s origins hail from the Institute of Physical and Chemical Research (known as RIKEN) headquartered in Wakō, Japan, in the 1930s. On March 15, 1939, the company was founded as Riken Keiki Co., Ltd, for the purpose of commercializing and mass-producing an optical interference gas detector that had been developed at the Institute. The company completed a factory in 1940 and an office in 1941 near the coal-rich Hokkaido region. Riken Keiki’s sensors were used to help detect gas in coal mines before serious explosions occurred, which were, unfortunately, common at the time.

During WWII, the company’s factories were commandeered by the Japanese as munitions production facilities. Post-war, the allied occupation restored Riken Keiki’s factories to producing gas detection equipment in order to promote further coal production to help Japan’s industrial era get back on track.

Over the following decades, Riken Keiki continued to develop gas detection and sensor technology. This included world-first innovations such as portable and belt-worn detectors. The company expanded beyond coal mines and entered oil & gas, automotive, food and beverage, and eventually semiconductors. The company expanded globally, opening new offices in North America, Europe, and Asia.

Over the decades, Riken Keiki developed more complex systems. Alongside individual hardware and sensor innovation, the company developed integrated systems incorporating controllers, multichannel alarm panels, and sampling systems, enabling centralized monitoring of dozens or hundreds of detectors in large plants. These larger systems increased switching costs for customers and created higher value‑added revenue, such as maintenance and repair services.

Business Model Today

Today, Riken Keiki continues to research, develop, manufacture, and sell industrial gas detection and alarm equipment, sensors, and systems. In addition, recurring maintenance services are also provided to customers. Riken Keiki’s main products include:

Stationary (fixed) gas detectors and alarm systems: combustible gas detection alarm systems, gas detector heads with signal converters, smart gas detector heads, single‑ and multi‑point indicator/alarm units, multipoint gas monitoring systems, fixed CO₂ monitors and gas analyzers.

Portable and personal gas detectors: multi‑gas detectors (e.g., GX‑9000, GX‑Force), single‑gas personal monitors, portable toxic gas monitors, gas leak checkers and six‑component gas detectors, often with Bluetooth connectivity, long battery life and rugged IP66/68 or explosion‑proof ratings.

Gas analysis and environmental measurement equipment: auto‑emission analyzers, surface analyzers (photoelectron spectrometers), optical gas indicators, calorimeters and environmental measurement devices used in laboratories, utilities and industrial process control.

Services and solutions: design and customization of gas sampling systems, installation, calibration, preventive maintenance, periodic inspections, sensor replacements and system upgrades, often delivered via long‑term service contracts and local affiliates.

It is notable that a key part of the business model revolves around replacing internal sensors more often than the equipment that houses them, resulting in hardware sales followed by recurring sensor sales. While equipment and hardware may last 5-10 years, internal sensors often require replacing every 6-18 months. This locks in customers to re-order sensors on a consistent basis and further incurs maintenance revenue, making this portion of revenue sticky and effectively recurring. Capital Light believes this is not appreciated by the current valuation.

Key Segments and Revenue Split

Riken Keiki discloses its revenue mix by device type, customer industry, and geography. The company also discloses mix by product and maintenance revenue.

Device type is split into three categories:

Fixed-Type: 63.6% of sales.

Portable-Type: 33.7% of sales.

Other measurement devices: 2.7% of sales.

Revenue by geography is split:

Japan: 44.1% of sales.

Asia (ex-Japan): 22.9% of sales.

North America: 16.7% of sales.

Europe: 3.9% of sales.

Other: 0.6% of sales.

Note: Riken Keiki’s investor presentation doesn’t disclose Japan revenue % mix directly. Number was calculated by taking all other regions and subtracting from 100%.

Revenue by customer industry is split:

Electrical and semiconductor: 41.1%

Petrochemical: 10.4%

Gas: 13.3%

Shipping: 6.1%

Other: 29.1%

Revenue by Product/Maintenance is split:

Products: 57.7%

Maintenance: 42.3%

Industry & Competition

The gas and alarm detection industry is moderately concentrated and characterized by several large global players alongside specialized regional firms. Prominent participants include Honeywell International, Drägerwerk, MSA Safety, Industrial Scientific, Siemens, Emerson, General Electric, Johnson Controls, New Cosmos Electric, Crowcon and others. Many of these companies offer broader safety, automation or instrumentation portfolios, with gas detection being one of multiple product lines. In contrast, Riken Keiki is more narrowly focused on gas detection and environmental measurement.

Market participants compete on sensor performance, reliability, compliance certifications, integration with control systems, total cost of ownership, and after‑sales service rather than on headline pricing alone, given the equipment’s mission‑critical nature.

Riken Keiki stands out in the industry due to being a reputable Japanese manufacturer, a long history of reliability, vertical integration including using the company’s own in-house designs (unlike some competitors), and specialization in high-value fixed systems as well as multi-gas portable instruments. Riken Keiki’s vertical integration allows it to control critical aspects of its supply chain that competitors may have less control over.

Key demand drivers applicable to Riken Keiki are clear. The first is the semiconductor industry CAPEX cycle. Historically, this has been a highly cyclical sector with boom and bust dynamics. AI narratives, however, appear to have stabilized the ‘boom’ cycle in the industry for now. Second is the petrochemical, oil, and gas sector, which remains highly cyclical and subject to geopolitical turmoil.

Other demand drivers include safety and environmental regulations (as regulations become more stringent, demand for monitoring increases), energy infrastructure growth, and technological advances enabling more robust feature sets, including IoT-enabled sensors, wireless connectivity, remote monitoring, and analytics capabilities.

Competitive Advantages

Riken Keiki’s competitive advantages include the following:

Research & Development, Technological depth, and in‑house sensors: Riken Keiki researches, develops, designs and manufactures its own sensors. Technology used includes electrochemical, catalytic, IR, optical interference, and optosonic. When done well, Riken Keiki can stay ahead of the competition that may not have the ability, resources, engineers, or budget to innovate.

Systems integration and high value‑added solutions: Beyond standalone detectors, Riken Keiki provides whole integrated systems and centralized monitoring. This embeds the company’s hardware in customer’s systems and makes Riken Keiki critically tied into customers’ operations.

Installed base and switching costs: Gas detection systems are safety‑critical, closely tied to plant layouts and often tied to regulatory approvals and customer procedures; replacing them involves engineering work, downtime and re‑certification, creating high switching costs once Riken Keiki’s equipment is installed.

Global approvals and vendor listings: Being placed on approved vendor lists of major corporations and holding certifications for international safety standards (e.g., for Aramco projects, marine approvals) forms an additional barrier for competitors trying to displace Riken Keiki in large accounts.

Global Scale: Riken Keiki benefits from being the largest specialized gas sensor company on the planet. Although global competitors include larger conglomerates like Honeywell and Siemens, these companies are more diversified and do not specialize in sensors. Riken Keiki’s niche focus on the sensor equipment market results in 100% of attention and resources being dedicated to that market, rather than having resources split amongst multiple business groups. Capital Light believes niche-dominant industry players have a natural advantage over more broadly diversified conglomerates.

Competitive Disadvantages and Risks

Larger Competitors: Despite Riken Keiki’s narrow and specialized focus, they still compete against larger firms with more absolute dollars. Should these larger competitors decide to act irrationally, they could potentially threaten Riken Keiki with a willingness to run unprofitably in the gas detection sensor market for an extended period of time.

Geographic concentration: Japan alone accounts for around 45% of revenue, exposing the company to domestic industrial and regulatory dynamics.

Geopolitical concerns: Although not disclosed precisely, China likely makes up a good portion of Riken Keiki’s Asia revenue (23% of total). Intensifying geopolitical tensions between western-allied Japan, western-allied Taiwan and China could result in sanctions and regulations that make it difficult to or prevent Riken Keiki from selling to the Chinese market.

Cyclical exposure: Significant exposure to the semiconductor, petrochemical, and gas industries results in potential headwinds from global economic cycles.

Financials & Valuation

Quick Valuation Metrics

As of the time of writing this piece, Riken Keiki’s stock price trades at ¥3540. It had traded as low as ¥2920 while working on this article. While I believe there is still strong value even at ~¥3500 per share, it was more attractive when it briefly sold off below ¥3000. Nonetheless, there is adequate upside to continue publishing this piece.

At ¥3500 per share, Riken Keiki has a market cap of ¥156B ($980M USD). The company holds around 16% of its market cap (¥25B) in cash and short-term investments, with little debt, bringing the enterprise value to ¥133B ($840M USD). Management has guided for ¥12B of EBIT in FY26 (FY26 ends on March 31, 2026). This gives the company a FY26 EV/EBIT multiple of 11. The company has earned ¥184 of EPS in the last twelve months, placing the trailing P/E at 19. Adjusting for the ¥550 per share in cash, the cash-adjusted P/E sits at 16.

Capital Light believes finding businesses of this quality for these multiples is extremely rare.

Profitability Analysis

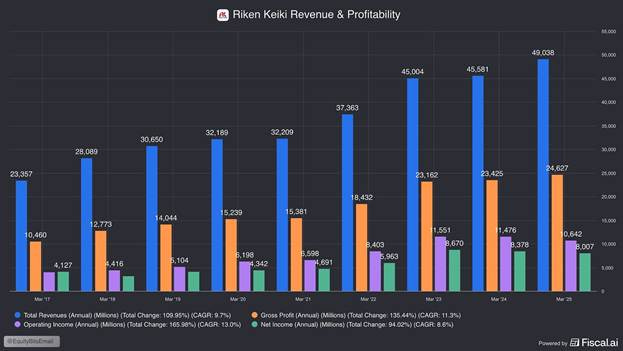

Riken Keiki’s revenue and profitability trajectory has been generally strong. Revenue has doubled since 2017 (9.7% CAGR), while gross profit and operating income have grown at 11% and 13% CAGRs respectively, maintaining a relatively steady upward trend. For FY26, management guided for ¥52B of revenue (+6% YoY) and ¥12B of operating income (+13% YoY), demonstrating clear operating leverage over FY25.

There is good reason to believe that Riken Keiki can maintain revenue growth in the mid single digits going forward in a base case scenario, with a path to double-digit revenue growth in a bull case. Global semiconductor equipment capex spending is expected to climb from $133B in 2025 to $156B in 2027 (8% CAGR). The oil & gas sector is more susceptible to the whims of the global economy, but even if infrastructure build-outs slow to a halt, Riken Keiki is likely to experience some growth from increased regulation and monitoring requirements. In the event of a burst of the semiconductor supercycle, Riken Keiki could experience a decline in revenue if not offset by other sectors.

Putting it all together, Capital Light believes a reasonable base case is 5–8% annual revenue growth with high single-digit to mid‑teens profit growth. A bear case would suggest downside to low single digit revenue declines in a macro/semi down‑leg. A bull case would have a path to 8–12% top‑line growth for a few years if AI‑driven fab capex and international expansion both hit at once. Modelling this out looks something like the following:

Riken Keiki’s conservative balance sheet has the capital to make the investments necessary to increase production inline with demand. The company spends about 6% of revenue on R&D, which is on the higher side for an industrial equipment company, suggesting that further innovation could drive upgrade cycles, coinciding with price increases and maintaining growth.

Capital intensity is low. Riken Keiki runs a structurally asset‑light model with modest capex needs resulting in solid free cash flow generation. Capex has ranged from just 2% to 12% of revenue in the past ten years. Revenue growth has followed CAPEX ramps in the following years.

Peer Comparison

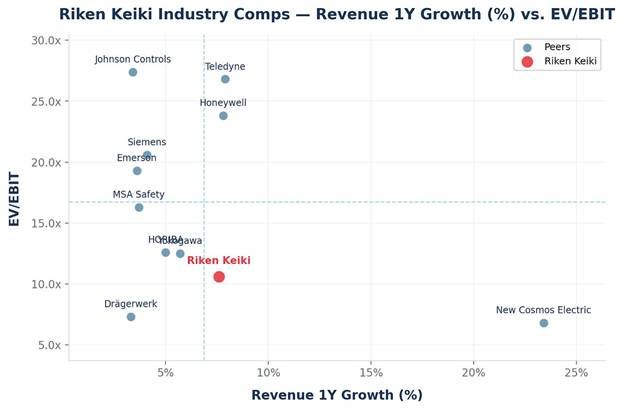

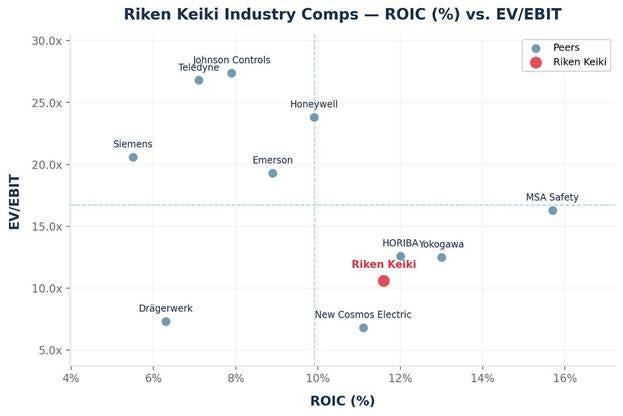

Relative to peers, Riken Keiki trades at modest multiples across the board. I had Claude generate scatterplots of trailing and forward valuation metrics vs. revenue growth, ROIC, and ROE. These scatterplots consistently illustrate Riken Keiki’s discount for its quality and growth rate relative to all major publicly traded peers. I’ve included a gallery with all the scatterplots at the bottom of this piece. I’ll highlight a couple in particular here. It is worth noting that most trailing and forward metrics are interchangeable, given the relatively mature nature of the industry.

The first chart shows Riken Keiki’s growth rate (TTM) of about 6%, putting it on par with American peers Teledyne and Honeywell. Despite this, Riken Keiki’s EV/EBIT multiple at about 11X is approximately half of Teledyne and Honeywell in the mid-20s. Slower-growth peers like Siemens and Emerson also find themselves at higher valuations.

The second chart was selected because it plots Riken Keiki’s ROIC relative to peers, illustrating the clear ‘cheap for the quality’ factor.

Quite frankly, all the Japanese companies are in a similar boat here, trading at considerable discounts to American and European peers, despite having superior growth and return metrics. This is a consistent theme across all the charts. Riken Keiki is perhaps the second most interesting. Direct competitor New Cosmos is actually more interesting, but is also much smaller. I have begun research on New Cosmos and will update readers in the future.

Conclusion

Capital Light rates Riken Keiki as a medium-conviction, low-to-medium-risk opportunity. This is a business with competitive advantages, durable recurring revenues, and a strong balance sheet. Investors are unlikely to lose a lot, and have the potential to make considerable gains if correct.

Valuation Scatterplots:

Sources:

Riken Keiki Investor Relations

Fiscal.ai

Claude

Thumbnail Image: Riken Keiki Product List

Disclosure: Accounts I manage are long Riken Keiki (7734)

Disclaimer: This post and all Capital Light posts are not financial advice in any way and should not be taken as such. All articles, including this one, and all information within Capital Light are for educational and informational purposes only. I receive no direct compensation from any company covered. I will likely profit in the event the share price of companies covered increases and I have a long position. I will likely profit in the event the share price of companies covered decreases and I have a short position. Although I make an effort to update readers when possible, I may choose to buy or sell at any time with no obligation to update or notify readers. Consult a professional financial advisor before making any investment decisions.

This is a useful overview of the topic

Great write-up Luke, enjoyed reading it.