Ongoing Coverage [Riken Keiki $7734]: FY2025 Update, Strong Growth, and Rapid Backlog Expansion

26% earnings growth and explosive 40% backlog growth at just a 12X EV/EBIT and 15X cash-adjusted P/E vs peers at 20X+

Hello Capital Light/Equity Bits readers!

Capital Light is becoming Equity Bits. This is a change I've wanted to make for a while. The new name better reflects the kind of coverage I want to write going forward. I still love asset-/capital-light businesses, but I want room to cover names that don't fit that mold, and to write shorter, punchier pieces, with greater frequency. Equity Bits fits that better.

It’s only been a month since Equity Bits (Capital Light at the time) pitched Riken Keiki (TSE: 7734), but the company has already reported strong earnings, resulting in the stock climbing to around ¥3700 per share, up a modest 5% from the original pitch price of ¥3500.

Equity Bits continues to believe there is near-term upside to ¥5000 per share as strong earnings results materialize into multiple expansion to a 16 EV/EBIT multiple.

Thesis Recap

Equity Bits pitched Riken Keiki on April 17, 2026 at ¥3500 per share. For those who need a refresher, here’s a quick recap:

Riken Keiki is a Japanese company that develops and sells gas detectors. This includes fixed detectors and integrated systems, as well as portable detectors. The company also provides ongoing maintenance and services revenue.

Riken Keiki’s revenue is split between Japan (53% of sales), China/Rest of Asia (24% of sales), North America (18% of sales), Europe (4% of sales), and Others (1% of sales).

Revenue mix by customer industry includes electrical and semiconductor (42% of sales), Gas & Petrochemical (23% of sales), Shipping (6%), and Others.

Generally, Riken Keiki sells equipment that lasts 10+ years. However, gas detection sensors housed within the equipment require replacement more frequently (sensors generally require replacement every 1-5 years, depending on the sensor), resulting in a razor-and-blades-like business model. Furthermore, jurisdictions like Japan require frequent inspection intervals mandated by law.

Equity Bits believes Riken Keiki is a high-quality business due to the recurring revenue components of sensor replacement and maintenance revenue.

Equity Bits thinks the market continues to underappreciate Riken Keiki. As a result, Equity Bits estimates +35% near term upside to ¥5000 per share as a base case, and as much as +90% upside to ¥7000 per share in a bull case.

FY25 Earnings Recap

Riken Keiki released FY25 earnings and a new medium-term management plan on May 13, 2026.

The highlights were as follows for the FY25 year (ended March 31, 2026):

Revenue ¥55.2B (+12.6% YoY)

Operating Profit ¥12.4B (+16.8% YoY)

Net Profit ¥9.96B (+24.4% YoY)

EPS ¥217 (+26.3% YoY)

Backlog ¥18.4B (+40% YoY)

Portable Device Orders +58%

Overseas Mix 47.3%

New ~¥5B buyback

These numbers landed well above management’s previously stated guidance of revenue of ¥52B (+6%) and ¥12B of operating profit. Overall, these are strong results, and the growing backlog continues to imply strong demand, particularly in semiconductors and data centers.

(Note: FY26 was labelled as FY27 in the original pitch. FY25 was April 1, 2025-March 31, 2026, while FY26 will be April 1 2026-March 31, 2027, hence we have now entered FY26.)

Medium-Term Plan & Targets

Management’s new medium-term plan, released alongside FY25 earnings, presented FY28 targets of ¥70B of sales and ¥14B of operating profit by FY28. The plan calls for a potential deliberate margin trough in FY27 or FY28 (though absolute operating profit is still expected to grow) from human capital and ERP investments. The margin plan likely reflects a mix of typical Japanese conservatism and genuine investment spend, but reiterates mid to high single-digit growth rates in revenue, with operating leverage starting to kick in near the end of the plan.

A Business Model Correction

In the original pitch, it was suggested that equipment lasts for about 10 years, while sensors housed within require replacing every 6-18 months. Upon further investigation, it appears the sensor replacement lifecycle is actually between 1 and 5 years. There is, however, a 6-month calibration interval mandated by Japanese law, that requires inspection and maintenance of gas detectors every 6 months. This is still a recurring maintenance revenue event, but not quite what was originally described.

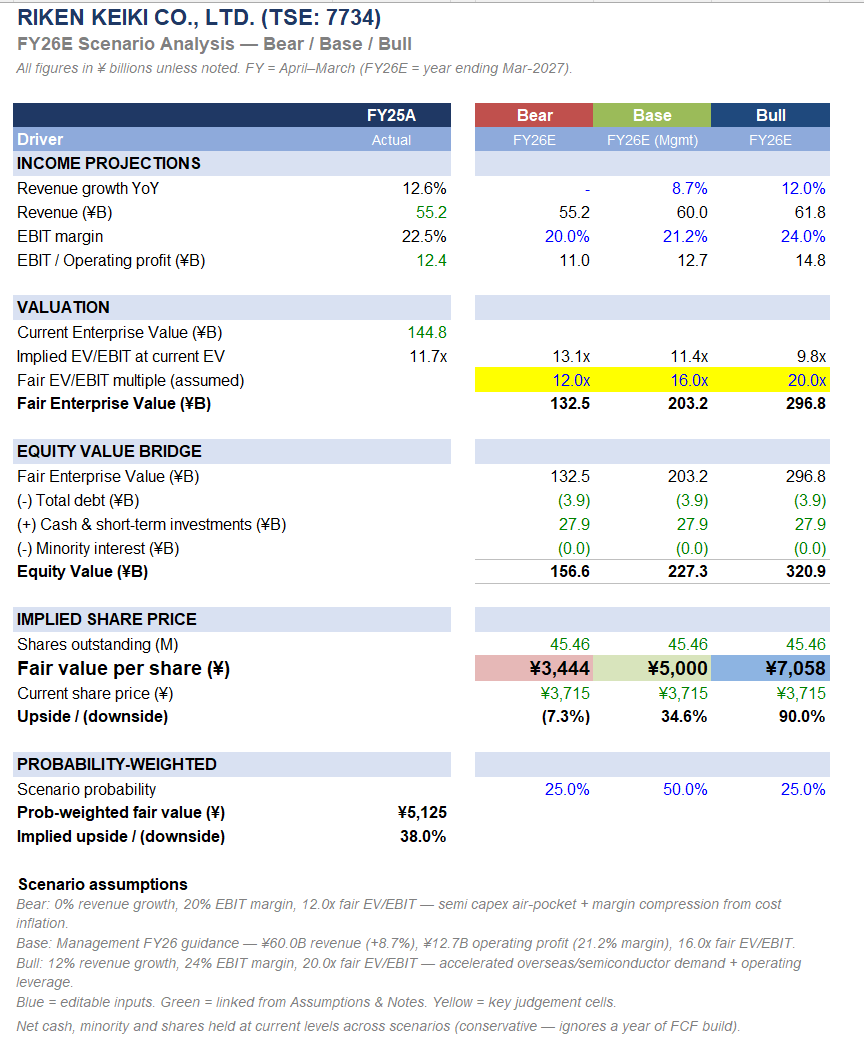

Update on Valuation

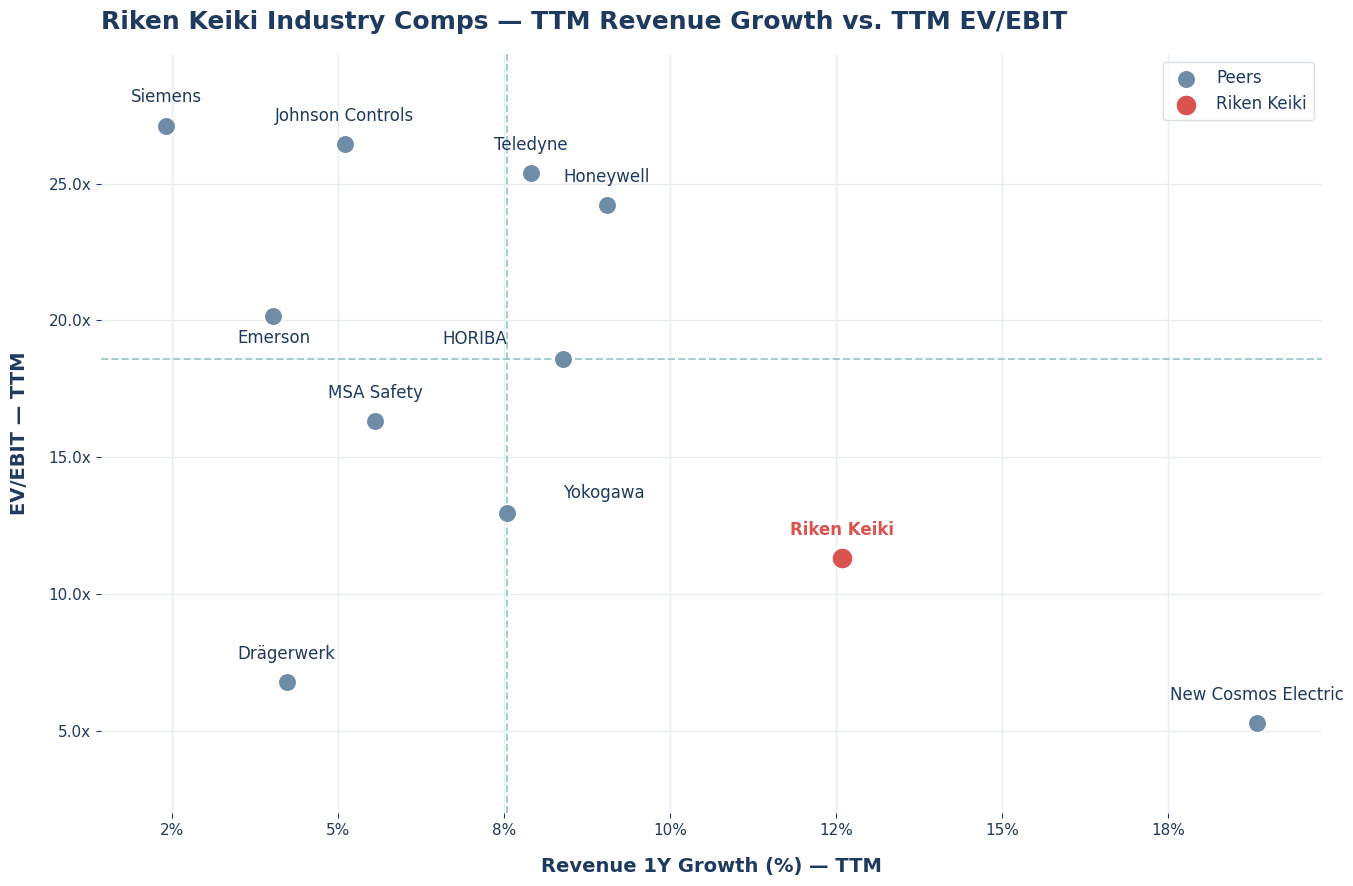

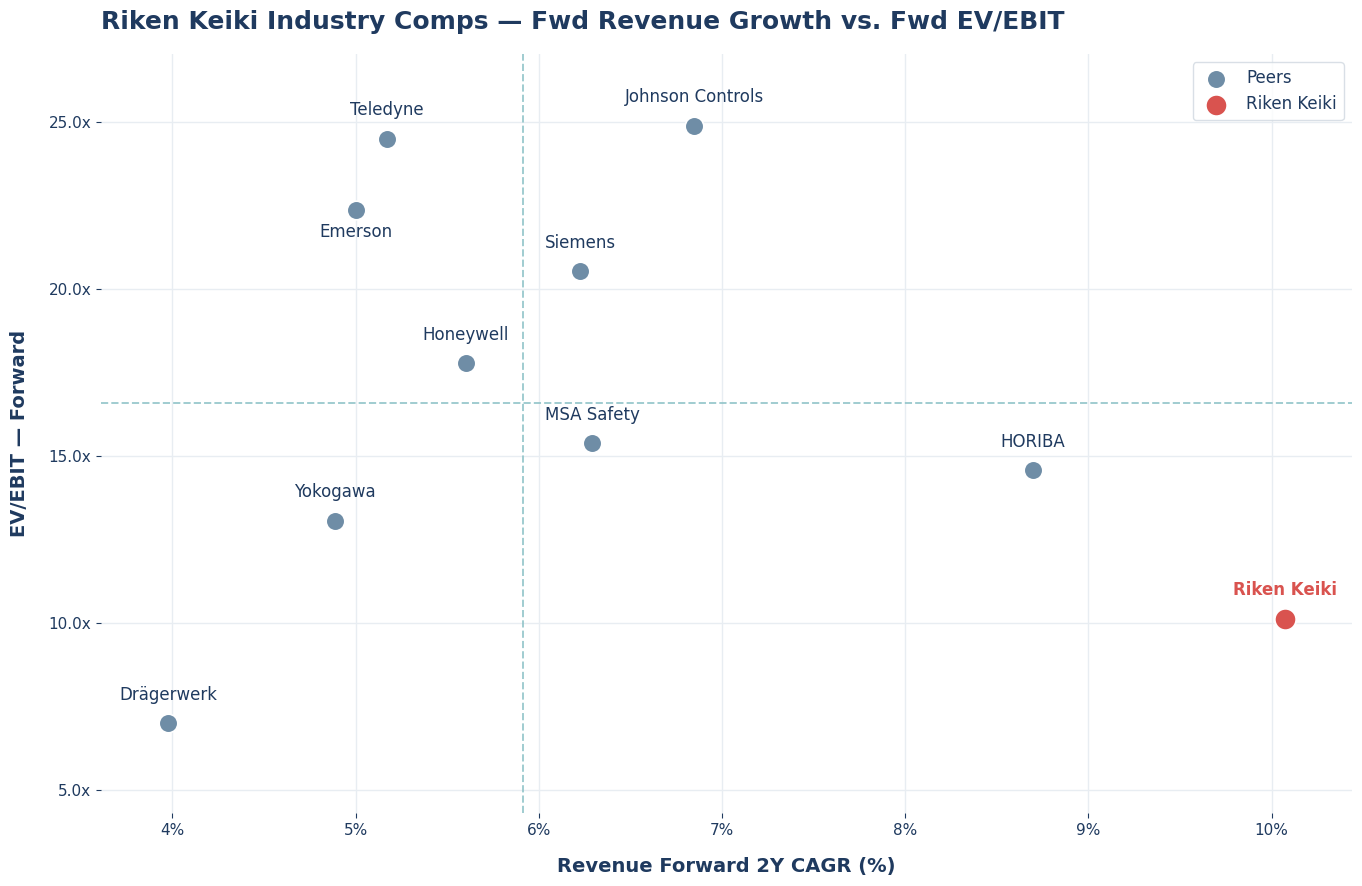

Equity Bits believes the stock price remains attractive, trading at multiples in the range of 60-70% of its Western peers, despite a dominant market position and leading market share. At an EV/EBIT of 11.7, Equity Bits believes there remains upside to a mid- to high-teens multiple, with long-term multibagger potential.

Updating cases for FY26 now that FY25 numbers have been released improves the base case slightly, raising the base case stock price from ¥4900 to ¥5000. The bear case improves from ¥3100 to ¥3400, and the bull case improves from ¥6900 to ¥7000.

The base case shown here is based on management’s numbers stated in the MTP and a 16 EV/EBIT multiple, while the bear and bull cases use EV/EBIT multiples of 12 and 20, respectively.

At the bottom, readers can find an Excel valuation model (created by Claude) with the above metrics, as well as a DCF and sensitivity analysis.

Updated scatter plots continue to tell the same story. Western peers trade at a median TTM EV/EBIT of around 18 (dotted line) vs Riken Keiki at under 12. The forward-looking picture tightens the dislocation narrative even further, placing Riken Keiki at the highest 2-yr forward growth rate (analyst estimates) of 10%, while at the same time, trading far below the 1-yr forward EV/EBIT of peers.

Conclusion

Overall, FY25 was a strong year, and 25FQ4 was a strong quarter. Management’s new medium-term plan provides new insight into what we can expect from the company over the next few years, including reiterating mid- to high-single-digit revenue growth rates, and is helpful in setting margin expectations.

Equity Bits continues to believe that Riken Keiki remains materially undervalued.

Files:

Sources:

Riken Keiki Investor Relations (see PDF files above)

Fiscal.ai

Claude

Thumbnail Image: Riken Keiki Product List

Disclosure: Accounts I manage are long Riken Keiki (7734)

Disclaimer: This post and all Capital Light posts are not financial advice in any way and should not be taken as such. All articles, including this one, and all information within Capital Light are for educational and informational purposes only. I receive no direct compensation from any company covered. I will likely profit in the event the share price of companies covered increases and I have a long position. I will likely profit in the event the share price of companies covered decreases and I have a short position. Although I make an effort to update readers when possible, I may choose to buy or sell at any time with no obligation to update or notify readers. Consult a professional financial advisor before making any investment decisions.